Recently, I have experienced an untoward incident of house repairs. An unexpected cost that required dipping into my emergency fund. Having never experienced something like this before, the entire experience was extremely stressful.

Even though I know deep down I’ve set aside an emergency fund – the psychological effect doesn’t quite align with that of rational budget planning. Having to use it makes me feel queasy, like I’m taking it out of my hard earned savings. EVEN THOUGH, the definition of emergencies in itself refers to cost you never quite anticipated.

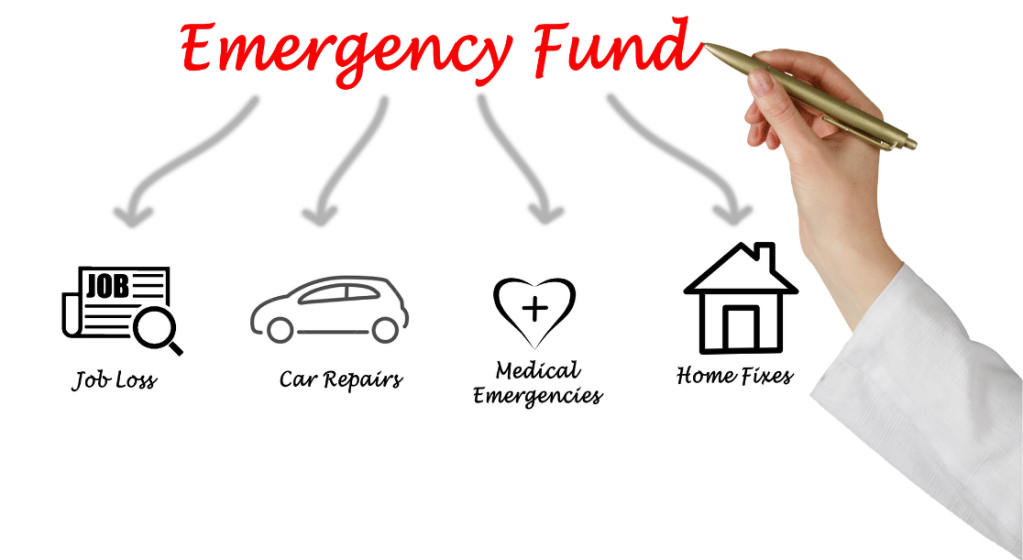

Admittedly when I think of these cost, I often think of it as money to keep afloat in a case of sudden unemployment and disaster when it should not be limited to that. Emergency funds are also intended to cover any cost resulting from unexpected events like:

- Medical emergencies for yourself/family or pet

- Unexpected home repairs

- Vehicle issues

- Unplanned home replacements

Emergencies are stressful as it is; the sense of lack of control is worrisome. Whether it arose from something out of your control or from your own ignorance (this applies for me on this occasion), all we can do is focus on the solutions and live and learn. You learn the best when the mistake is costlier.

Shit happens often so better save it for a rainy day.

Rule of thumb for emergency funds:

To be safe, you should have about 6 months worth of living expenses emergency funds set aside.

This means your essential expenses, the cost you require to sustain yourself which includes:

- Housing (mortgage or rent)

- Food

- Healthcare (including insurance)

- Utilities

- Transportation

- Debt repayment

- Pet expenses

- Other lifestyle expenses (though bear in mind, in an emergency, lifestyle expenses should be kept to the bare minimum)

Non-essential expenses can be omitted from this list however, it is your personal choice to decide how conservative you’d want to be. At the VERY minimum, it should cover all of your essential expenses but if you’d like to include a margin of safety based on your risk appetite, by all means go ahead.

There are special considerations to this, which varies from situation to situation. Maybe it’s good to beef up the fund in a recession, or if your job scope is pretty risky, you are in a phase of your life that much is going on. So remember to tailor it to your current situation.

If you end up drawing into it, remember to make concrete plans to build back up the fund again which either means directing all your savings to the fund for a temporary period of time before deciding to invest or repay your debt.

Because this is an emergency fund, WHERE you stash this money is also extremely important. Criteria on your choice of storage includes:

- Accessibility – you can gain access to it quickly, with minimal to no turnaround time required

- Liquidity – where the cost of withdrawing the money bears minimal to no penalty

- Stability in value – where the nominal value of how much you have stashed away remains stable

- Safe – protected from theft and breaches of security

This means the preferred options are:

- In a separate interest bearing personal bank account

- In a fixed deposit

- In a cash management portfolio from roboadvisors (such as Stashaway Simple)

or a combination of the above. There are many pros & cons to each option so remember to do your own due diligence before making a financial decision.

Remember, the emergency fund comes first.

Pro tip to reduce the impact of emergencies: Ask Around

If it’s an emergency, chances are you have limited experience in the matter. So it’s good to ask around to consult any friends who may have experienced the same issue or may be able to offer some good advice. After all, being in a stressful situation, we are often blinded by what’s in front of us, so an extra opinion always helps. I’m so grateful for the support, advice and help my friends have extended to me, it made the world’s difference.

If none of your friends know of it, there’s always google. Scour the net for frequently asked questions, forums on things to look out for.

Here’s to preparedness in life, learning from mistakes and being able to handle what life throws at us.

Disclaimer: I’m not a professional financial advisor and this is not financial advice. I’m just sharing based on what I learned in my own journey and I hope it inspires you to learn more too.